Incorporate in Cyprus.

Structure Smarter.

Cyprus is one of the most tax-efficient business jurisdictions in the European Union — a 15% corporate tax rate, zero withholding on dividends to non-residents, an IP Box regime, and a non-dom status that can eliminate personal SDC on investment income for up to 17 years. All within a fully legal, EU-compliant, OECD-aligned framework. We handle the entire setup.

-

Corp. Tax

15%on worldwide profits

(effective 1 Jan 2026) -

Dividends Out

0%withholding to non-

residents (most cases) -

Dividends In

0%on foreign subsidiary

dividends (participation exemption,

subject to conditions) -

Capital Gains

0%on share disposals

(except Cyprus real estate) -

IP Box

~3%effective rate on

qualifying IP income

(80% exemption × 15%) -

Non-Dom

0%SDC on dividends &

interest for up to 17 years -

Tax Treaties

70+double tax treaty

arrangements -

Setup Time

5-10working days

-

Annual Fee

Abolishedfor Cyprus companies

from 2024 onwards

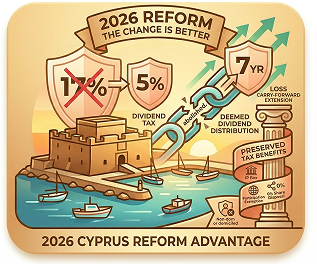

The Cyprus Tax Framework — What You Need to Know.

Cyprus enacted its most comprehensive tax reform in over 20 years on 22 December 2025, effective 1 January 2026. The headline change was an increase in corporate income tax from 12.5% to 15% — aligning with OECD Pillar Two minimum tax requirements. What was preserved is equally important: every major exemption and incentive that has made Cyprus attractive to international businesses remains fully in force.

The numbers that matter: zero withholding on dividends paid to non-resident shareholders in most cases, zero capital gains on the sale of shares, ~3% effective rate on IP income through the IP Box, zero SDC on dividends and interest for non-dom residents for up to 17 years, and a network of 70+ double tax treaty arrangements.

2026 Reform — also changed for the better: SDC on dividends for domiciled Cyprus residents reduced from 17% to 5%. Deemed dividend distribution abolished for 2026 profits onwards. Loss carry-forward extended from 5 to 7 years. The IP Box, participation exemption, 0% on share disposals, and non-dom status are all fully preserved.

Four Clients. Four Different Situations. One Island.

The clients below are composite examples based on the types of situations we help with regularly. Names and details are illustrative. Every situation is unique — these stories show how the different elements of

Cyprus's tax framework come together in practice.

Daniel

IT Consultant from Canada — €120,000/year

Daniel had been invoicing his US client directly as a sole trader from Toronto for six years, paying over 50% in combined federal and provincial tax. He relocated to Cyprus, established a Cyprus private limited company, and his US client now engages the company rather than Daniel personally. The company pays 15% corporate tax. Daniel draws dividends — which, under non-dom status, carry zero SDC in Cyprus. He lives well, pays substantially less tax, and works exactly as he did before — just from a better climate.

Income / Revenue€120,000

Tax~€62,000(income + social)

Net Kept~€58,000

Maya & Tom

SaaS Founders from the UK — €500,000/year

Maya and Tom were generating €500,000 a year in licensing revenue, incorporated in the UK at 25% corporate tax with no IP relief. By incorporating in Cyprus and housing qualifying IP in the Cyprus company with genuine R&D performed on the island, 80% of their qualifying IP income became exempt from corporate tax. The remaining 20% is taxed at 15%, giving an effective rate of approximately 3%. Dividends carry zero withholding tax.

Revenue€500,000

Tax~€143,750

Net Distributed~€356,250

Viktor

Business Owner — €400,000/year in upward dividends

Viktor runs three operating companies in Poland, Romania, and Bulgaria. By restructuring through a Cyprus holding company, dividends received from foreign subsidiaries are generally exempt from Cyprus corporate tax under the participation exemption. Zero withholding tax applies when profits are distributed to Viktor. Any future sale of shareholdings carries zero capital gains tax. Viktor has established tax residency in Cyprus and benefits from non-dom status.

Dividends Received€400,000

Total Tax~€102,500

Net to Viktor~€297,500

The Müller Family

Trading Business from Germany — €300,000/year

Klaus and Petra ran a second-generation trading business in Bavaria. Between German corporate tax, trade tax, and personal tax on distributions, they were keeping less than half of what the business earned. They relocated to Cyprus, re-established the trading company in Limassol, and built genuine operational presence on the island. Corporate tax: 15%. Dividends under non-dom: zero SDC. Cyprus imposes no inheritance tax. The family's quality of life has materially improved. So has their balance sheet.

Total Tax~€142,500

Net Retained~€157,500

— plus a significantly improved quality of life.

What We Handle — Start to Finish

Company Incorporation

Name approval, M&A, filing with the Registrar. 5–10 working days.

Tax Structure Advice

We connect you with qualified Cyprus tax advisors to confirm the right structure.

Corporate Banking

Introduction and facilitation of corporate bank account opening, subject to KYC compliance.

Tax & VAT Registration

Tax ID and VAT registration where applicable.

Accounting & Annual Audit

All Cyprus companies must file audited accounts annually. We coordinate with licensed auditors.

Immigration & Residency

For owners and staff relocating to Cyprus, we coordinate permits and tax residency alongside company setup.

Ongoing Compliance

Annual returns, beneficial ownership filings, tax filings, and structural changes.

Premium Bookkeeping & Payroll

Day-to-day financial management, including transaction recording, reconciliations, expense tracking, payroll processing, and real-time reporting.

How the Process Works

-

Free Consultation

We understand your business model, income sources, and goals — and give you a clear picture of which structure applies, what it costs, and what it involves. No obligation.

-

Tax Structure Confirmed & Name Approved

A qualified Cyprus tax advisor confirms the right structure. Company name submitted to the Registrar. Typically 1–3 business days.

-

Documents Prepared

Passport copies, proof of address, source of funds declarations, and beneficial ownership information — all certified and prepared.

-

Incorporated

Memorandum and Articles of Association prepared by a licensed Cyprus lawyer, filed with the Registrar. Certificate of Incorporation typically issued in 5–10 working days.

-

Registered, Banked & Operational

Tax Department registration, VAT where applicable, and corporate bank account facilitated. Most setups are fully operational within 3–6 weeks of starting.

What a Cyprus Company Requires

Shareholders

Minimum 1 any nationality.

100% foreign ownership permitted.

Directors

Minimum 1 Management and control must be genuinely exercised in Cyprus for tax residency — Cyprus-resident board majority is the standard approach.

Company Secretary

Mandatory individual or corporate secretary required.

Registered Office

Physical registered office address in Cyprus required. We provide this.

Annual Audit

All Cyprus companies must prepare and submit audited financial statements annually.

Annual Company Fee

Abolished from 2024. Ongoing costs: registered office, accounting, audit, compliance.

Substance is essential:

For a Cyprus company to be tax resident in Cyprus — and access the treaty network and the 15% rate — management and control must be genuinely exercised from Cyprus. Real directors, real decisions, real meetings on the island. We advise on this from day one.

Common Questions.

-

Has the 2026 tax reform made Cyprus less attractive?

No. The rate increased from 12.5% to 15% to align with OECD Pillar Two. What was preserved is equally important: 0% withholding on outbound dividends to non-residents, 0% capital gains on share disposals, IP Box (~3% effective rate), participation exemption, non-dom regime, and 70+ treaty network. The reform also brought improvements — SDC on dividends for domiciled residents reduced from 17% to 5%, deemed dividend distribution abolished, and loss carry-forward extended from 5 to 7 years.

-

What is the IP Box and does my business qualify?

The IP Box provides an 80% exemption on qualifying income from IP — primarily patents and copyrighted software. At 15% corporate tax, the effective rate is approximately 3%. The IP must meet the OECD BEPS nexus approach — R&D must genuinely be performed in Cyprus.

-

Can I open a bank account without coming to Cyprus?

In most cases, corporate bank account opening requires the physical presence of at least one director for KYC. We prepare clients thoroughly and accompany the process at every stage.

-

What are the ongoing annual costs?

The annual company levy was abolished from 2024. Ongoing costs include registered office, accounting, audit, tax return preparation, and director/secretary fees where applicable. A straightforward company typically runs €2,000–€5,000 per year in total professional fees.

Not Sure Where to Start?

Most people come to us with one question and leave the first conversation with a clear

plan. Tell us your situation and we will tell you which permit applies, what it involves,

and what the next step looks like.

WHATSAPP

+1 855-425-0946

Fastest response - Available 7 days

EMAIL

success@thecyprusadvantage.com

We reply within one business day

book online

Schedule a Call

Choose a time that works for you